Hyperliquid activated HIP-4 on mainnet on May 2, 2026, four days after Polymarket shipped its CLOB V2 and $pUSD migration. Both upgrades landed in the same week. That is not a coincidence.

We covered the mechanism in What Is Hyperliquid HIP-4 when the spec was first published. This post is about what actually shipped, what is still unresolved, and the four signals that resolve the thesis over the next 90 days.

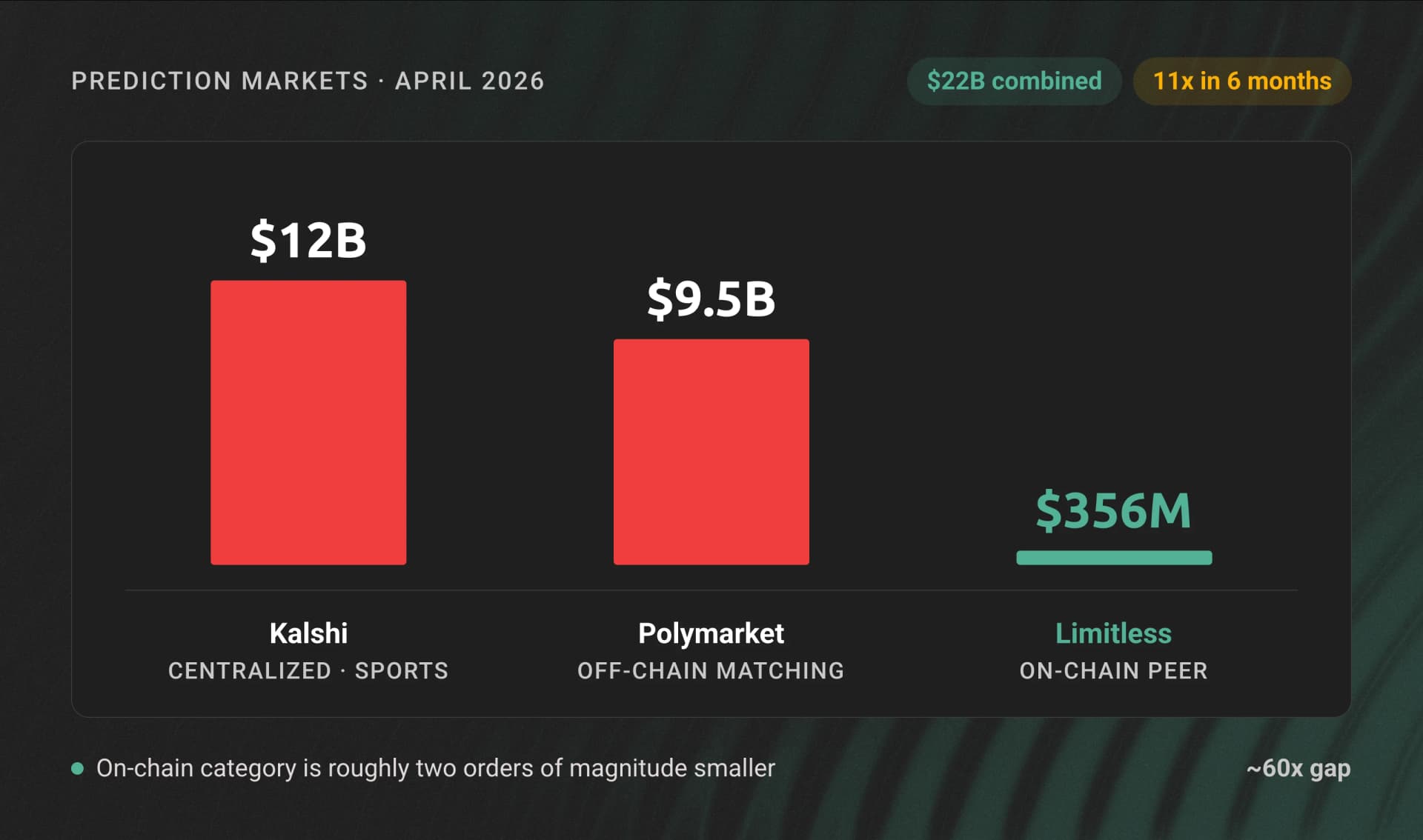

The category just got real

Polymarket and Kalshi printed $22B of combined volume in April 2026. The category 11x'd in six months. Sports drove Kalshi to $12B for the month. Geopolitics carried Polymarket to $9.5B. Limitless, the closest on-chain comparable, crossed $356M.

The on-chain segment is two orders of magnitude smaller than its centralized counterpart. That gap is the bet HIP-4 is making.

What HIP-4 actually is, in one paragraph

A binary contract. Trades between 0.001 and 0.999. Settles to 0 or 1. Fully collateralized in USDH. Same shape Polymarket and Kalshi use. What is different is everything around it.

HIP-4 markets are dated. They open with a roughly 15 minute clearing auction (borrowed from equities, prevents the first trade from setting an arbitrary anchor). They run on the same CLOB engine as Hyperliquid perps. They settle to USDH on-chain.

The first market on mainnet is a recurring daily BTC binary. One 1M HYPE stake. Hundreds of recurring daily contracts. Slot recycling amortizes the capital cost across the entire series.

Why HIP-3 could not have done this

Hyperliquid already supports permissionless perp deployment via HIP-3. The reasonable question is why HIP-4 needs to be its own contract type at all.

HIP-3 clamps mark price updates at 1% per oracle tick. That is the right design for a $WTIOIL or $TSLA perp. It is a disaster for a contract that needs to settle from 0.50 to 1.00 the instant an event resolves.

Under that constraint, the mark price would need roughly 50 sequential ticks to reach the true settlement value. That is 50 minutes of guaranteed risk-free profit for anyone watching.

HIP-4 sidesteps it entirely. Linear interpolation around the expiry timestamp. Authorized oracle posts the binary outcome. Optional dispute window. Instant resolution.

The mechanism is the product.

Three things only HIP-4 does

| Capability | HIP-4 | Polymarket V2 | Kalshi | Limitless |

|---|---|---|---|---|

| Cross-margin with perps and spot | Yes | No | No | No |

| End-to-end on-chain (order, match, settle, oracle) | Yes | Off-chain matching | None | Partial |

| Permissionless market creation | Yes (1M HYPE stake) | No | No | Yes |

| Maker rebate | None | 20-25% of taker fees | Yes | Varies |

Cross-margin with perps and spot. A long BTC perp plus a "BTC > $80k by Friday" outcome contract sharing the same USDH collateral. Polymarket lives on Polygon. Kalshi lives in a brokerage account. No prediction market venue has unified margin with leveraged perps. None.

On-chain end-to-end. Polymarket's V2 still matches off-chain. Kalshi has no chain at all. HIP-4 runs every step on HyperCore: order, match, settle, oracle.

Permissionless deployment via burnable stake. 1M HYPE, slashable, burned on slash. Up to 50% builder fee share above the base rate. Phase 2 turns market creation into a deployable revenue line, not a curated listings function.

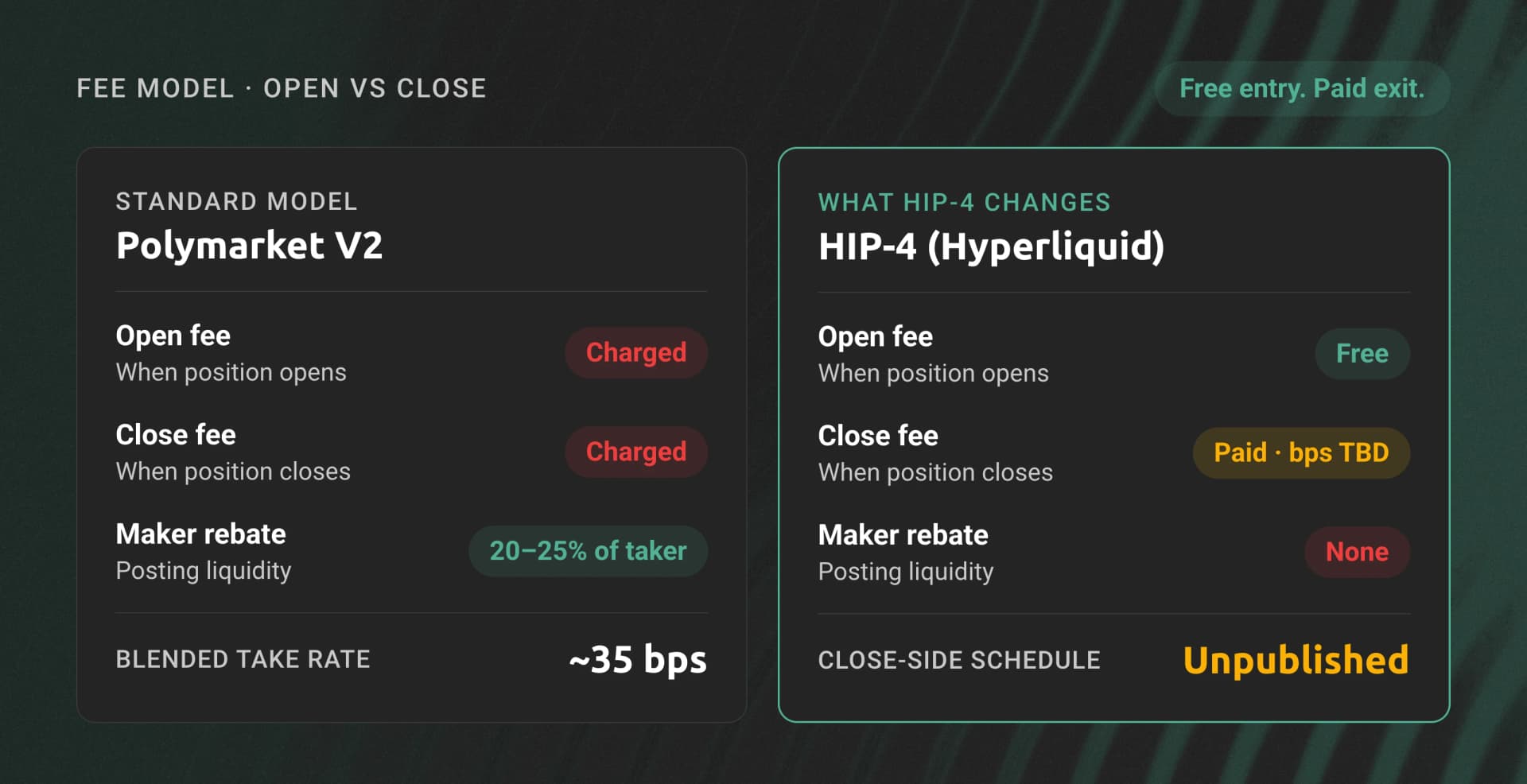

The fee asymmetry no one else does

HIP-4 ships with zero maker rebate. Polymarket pays makers 20 to 25% of taker fees. HIP-4 pays them nothing. Pure spread capture for makers.

The other axis is more interesting. Fees apply only on close, not on open.

Free entry. Paid exit.

That changes the calculus on market making and on holding to settlement. Polymarket's blended take rate is roughly 35bps on volume, $28M April fees on $8.1B. HIP-4's close-side number is not yet published. It could land anywhere from 5 to 50bps. Until that schedule is public, every revenue projection for HIP-4 markets is fiction.

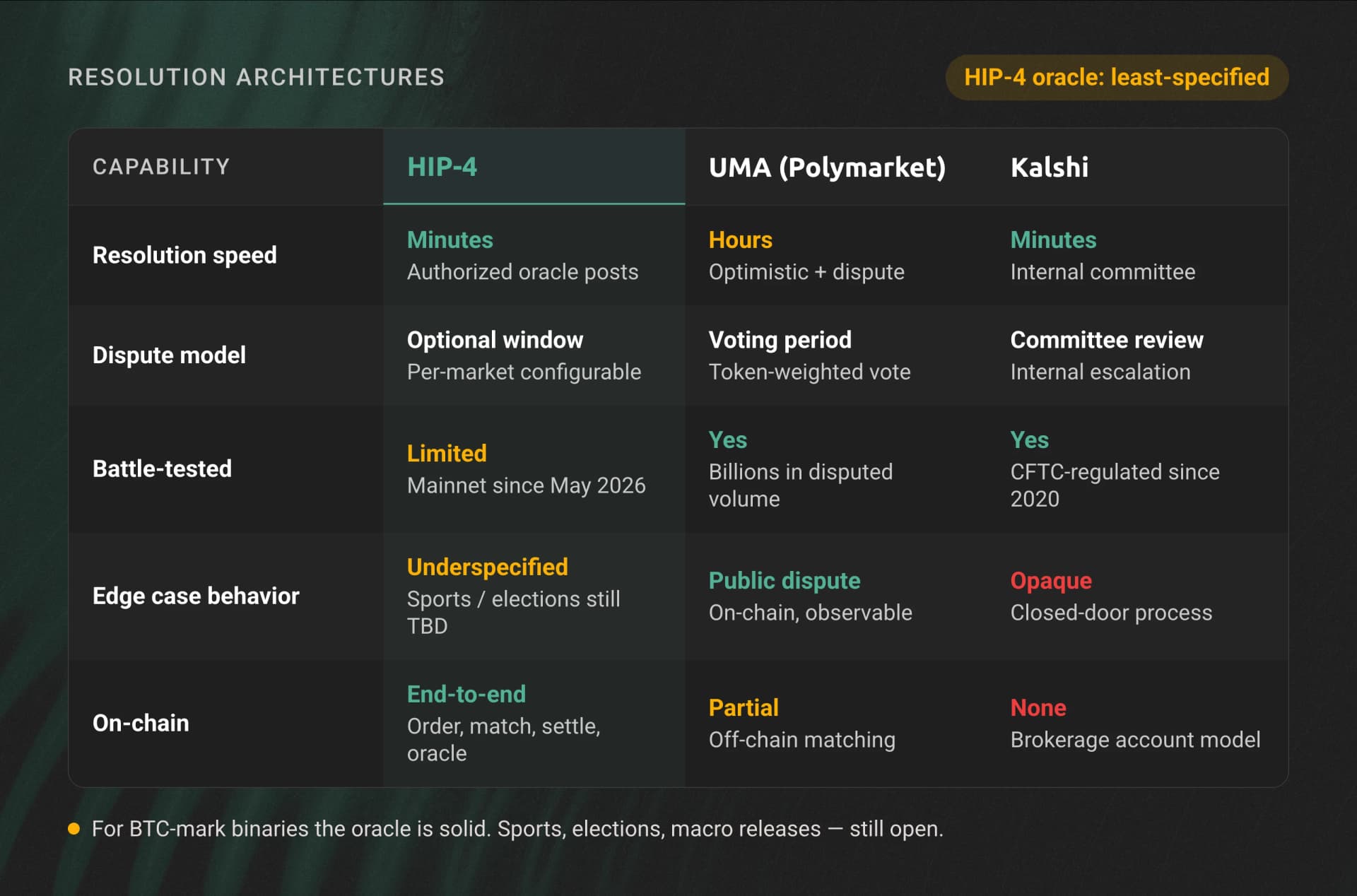

Speed has a cost

Three resolution philosophies are now competing for the same volume:

- HIP-4: authorized oracle, minutes-bounded resolution. Fast in the common case. The architecture is the least-specified part of the spec.

- UMA optimistic oracle (Polymarket). Slower. Battle-tested across billions in disputed volume.

- Kalshi committee. Fast in the common case. Inscrutable in the edge case.

The honest framing on HIP-4: for the BTC daily binary, the oracle is HyperCore's mark price. Years of operational data. Solid.

For sports, elections, and macro releases, the oracle infrastructure has not been publicly designed. There is room for deployers to choose different oracles, similar to how HIP-3 works. That flexibility is also a known unknown until builders start shipping.

Arc and the first ecosystem build

Kinetiq and Markets are building Arc, framed by the team as "the endgame for onchain outcomes." Markets is the largest USDH-denominated HIP-3 DEX. Kinetiq accounts for over 95% of CoreWriter precompile transactions on HyperEVM.

Arc is the first application stack to cover deployment (HIP-3 plus HIP-4 via Markets, powered by kmHYPE), distribution, and frontends through builder codes. Watch what they ship as the test case for whether HIP-4 stays a Hyperliquid feature or becomes a category.

What infrastructure breaks first

A few things to plan around if you are building on HIP-4:

- Settlement spikes. Hundreds of recurring daily contracts settle around the same UTC boundary. Public endpoints rate-limit at 100 requests per minute. Production read paths need dedicated infrastructure to clear the spike.

- Oracle posting latency. Authorized oracles need consistent block-inclusion to keep resolution windows tight. For a binary that needs to flip 0.50 to 1.00 instantly, an extra 600ms of inclusion lag is a real problem.

- Cross-margin reads. Cross-margin with perps and spot means your risk engine needs a single consistent view of perp positions, spot balances, and outcome positions. Polling three endpoints and reconciling is not the answer at production scale.

- Builder code paths. Phase 2 deployment leans on builder codes. WebSocket and gRPC support matter more than REST as builder-driven flow grows.

This is the infrastructure layer Dwellir runs on Hyperliquid. If you are deploying an HIP-4 market or building a frontend against one, contact the Dwellir team to talk through the read-path and oracle posting setup.

Four signals that resolve the thesis in 90 days

- Close-side fee bps. The actual number, published. Without it, no one can price market making honestly.

- Daily BTC binary volume vs Polymarket's BTC 24h price markets. The cleanest head-to-head comparison HIP-4 will ever get.

- Phase 2 transition timing and the first independent builder. The category they pick tells us whether HIP-4 is a separate product or a Hyperliquid feature.

- Portfolio margin GA. Cross-margin is the headline. Without portfolio margin in production, the headline does not ship.

HIP-4 is not trying to beat Polymarket on Polymarket's turf. It is trying to be the venue where event contracts share collateral with leveraged perps, where market creation is a permissionless revenue line, and where every step settles on-chain.

That is a different product. The mechanism works. The question is whether the market wants it.

The next 90 days resolve that.

For teams building on Hyperliquid who need infrastructure that holds up through settlement spikes and oracle posting windows: Get started with Dwellir →