Cross-border payments cost $25-35 per transaction and take 2-5 days to settle. That pricing has barely moved in decades, even as the underlying volume reached $150 trillion annually. Stablecoins settle the same payments in seconds for fractions of a cent.

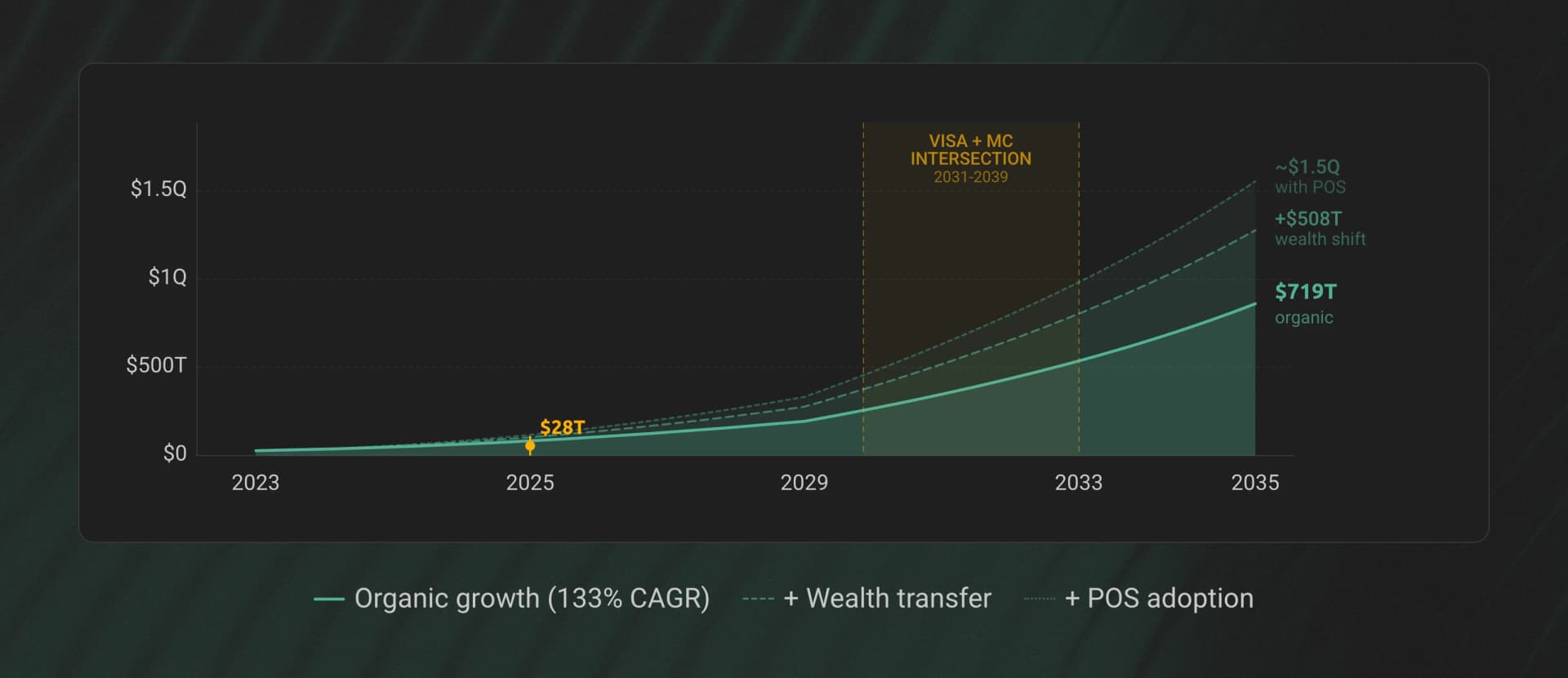

In 2025, stablecoins processed $28 trillion in adjusted on-chain volume. Not speculative trading volume. Real economic activity - supplier payments, payroll, treasury transfers, settlement. That figure grew at a 133% compound annual growth rate since 2023, and the composition tells you where this is heading: 60% of stablecoin payment volume now comes from B2B transactions, with B2B stablecoin payments surging 733% year-on-year according to McKinsey.

This is not a crypto story anymore. JPMorgan, Visa, Stripe, Wells Fargo, Mastercard, and SWIFT have all made production-grade stablecoin commitments in the past 12 months. Stripe built an entire blockchain for it. The institutions that move the global financial system are shipping, not piloting.

The Stablecoin Moment: Why 2026 Is Different

Total stablecoin supply reached $316 billion by April 2026, up 54% from $205 billion at the start of 2025. Tether (USDT) commands 58% of the market at $176-180 billion. Circle's USDC holds 25% at $73-77 billion. Together they represent more than 93% of total supply.

Usage, not market cap, is what separates this moment from previous crypto cycles. Monthly USDT transaction volume routinely exceeded $703 billion through H1 2025, peaking at $1.01 trillion in June. USDC quarterly on-chain transaction volume hit $11.9 trillion in late 2025 - a 247% increase year-over-year. Active stablecoin wallets grew 53% to 30 million.

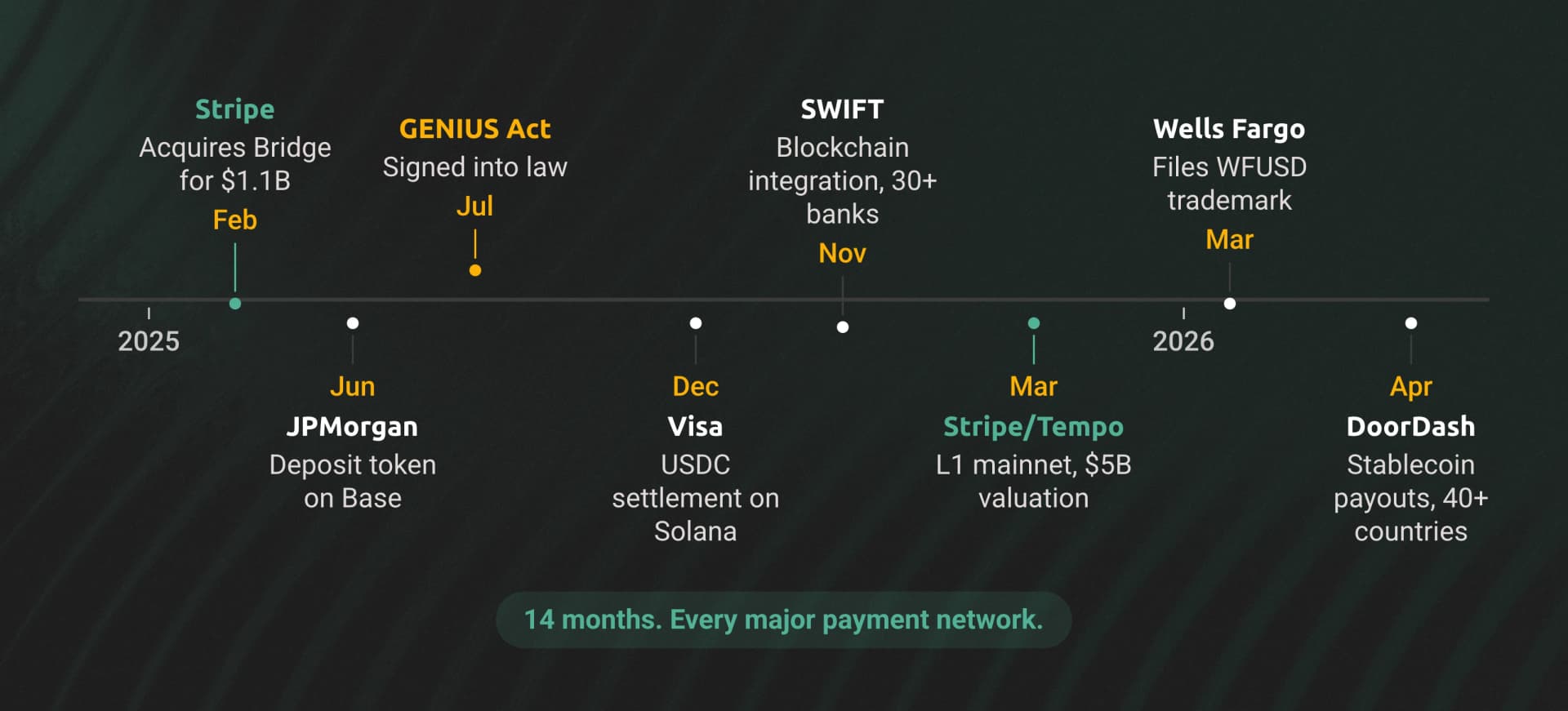

Enterprise intent has moved past curiosity. Fireblocks surveyed 295 global institutions and found that 49% actively use stablecoins for payments, with another 41% in piloting or planning stages. Only 10% remain undecided. The acquisition activity confirms it: Stripe's $1.1 billion Bridge deal and Mastercard's $1.8 billion BVNK acquisition are bets on stablecoin infrastructure as core payments plumbing.

The projections reflect this trajectory. Bernstein forecasts a $4 trillion stablecoin market by 2035. Treasury Secretary Bessent has projected $2-3.7 trillion by end of decade. Chainalysis models adjusted stablecoin volume reaching $719 trillion by 2035 through organic growth - surpassing global cross-border payment volumes today.

Three Catalysts Converging

Three forces are converging in 2026 that did not exist together before: regulatory frameworks, bank participation, and a generational demand shift. Each one removes a different barrier to enterprise adoption.

Regulatory Clarity

The GENIUS Act was signed into US law on July 18, 2025, passing the Senate 68-30 and the House 308-122. It provides the first federal regulatory framework for payment stablecoins: 100% reserve backing with liquid assets, monthly public disclosures of reserve composition, and Bank Secrecy Act compliance for issuers.

In Europe, MiCA hit full enforcement for all crypto-asset service providers in December 2024, with the final 18-month grandfathering period ending July 1, 2026. The result is measurable: MiCA-compliant businesses saw a 45% increase in institutional investments compared to non-compliant platforms. Singapore, Hong Kong, Japan, and the UAE all enacted stablecoin-specific regulatory frameworks in 2025, opening institutional markets across the Asia-Pacific region.

For enterprises that needed legal clarity before deploying capital, the regulatory question is answered.

Traditional Finance Goes Live

The direction of adoption has flipped. Banks are building stablecoin products, not responding to pitches from crypto companies.

JPMorgan launched a deposit token proof-of-concept on Coinbase's Base network in June 2025 and expanded to the Canton Network. Its Kinexys blockchain platform processes $2 billion daily, with clients including Coinbase, Mastercard, and Siemens.

Wells Fargo filed its "WFUSD" trademark with the USPTO in March 2026. Bank of America CEO Brian Moynihan confirmed active stablecoin capability development. Citigroup CEO Jane Fraser confirmed exploration of a "Citi stablecoin" alongside tokenized deposits.

A May 2025 Wall Street Journal report revealed that JPMorgan, Bank of America, Citigroup, and Wells Fargo held discussions about jointly launching a stablecoin, potentially using the infrastructure behind Zelle and The Clearing House.

The payment networks are moving at the same pace. Visa launched USDC settlement for US banks in December 2025 following a $3.5 billion annualized pilot, and now has 130+ stablecoin-linked card issuing programs in 40+ countries. SWIFT launched blockchain integration in November 2025, with over 30 financial institutions - HSBC, BNP Paribas, BNY Mellon, Ant International - engaged in pilots.

Stripe's moves are the most telling. After acquiring Bridge for $1.1 billion in early 2025, Stripe went further: it incubated Tempo, a purpose-built Layer 1 blockchain designed from the ground up for stablecoin payments. Co-developed with Paradigm and led by Paradigm co-founder Matt Huang, Tempo raised $500 million at a $5 billion valuation and went live in March 2026. Visa signed on as an anchor validator. DoorDash partnered to offer stablecoin payouts to merchants and delivery workers across 40+ countries. Fifth Third Bank, Coastal Community Bank, and Howard Hughes Holdings are bringing payments operations onto the chain. Tempo will serve as Stripe's primary blockchain infrastructure for worldwide payment operations - meaning the company that processes payments for millions of internet businesses is now routing those payments through its own stablecoin-native chain. That is not a pilot. That is a platform bet.

The Generational Wealth Shift

Between 2028 and 2048, an estimated $100 trillion in wealth will transfer from Baby Boomers to Millennials and Gen Z. A 2025 Gemini survey found nearly 50% of Millennials and Gen Z have held or currently hold crypto.

This is a 20-year structural demand curve. As capital moves to generations with native comfort in digital assets, the share of global financial activity flowing through stablecoin rails grows with each transfer cycle.

Where the Business Value Is

Six use cases account for most enterprise stablecoin volume today, each driven by measurable improvements over existing financial rails.

Cross-Border B2B Payments

Traditional correspondent banking moves $150 trillion annually through a system that charges $25-35 per transaction and settles in 2-5 days. KPMG's October 2025 report found stablecoins reduce these costs by up to 99%.

Speed has overtaken cost as the primary driver. Fireblocks found 48% of enterprises cite settlement speed as their top adoption motivator, ahead of cost savings at 30%. EY's enterprise survey found 77% of organizations named cross-border supplier payments as their top stablecoin application.

The volumes back this up. Zeebu, a telecom settlement platform, processed $5.7 billion in stablecoin B2B payments. B2B stablecoin payment volumes surged 733% year-on-year. Asia accounts for 60% of global stablecoin payment volume - $245 billion in 2025 - driven by Tron-based USDT for B2B settlement.

Treasury Management

Stablecoins let enterprises manage liquidity across global subsidiaries without local bank accounts or currency conversion delays. Siemens uses JPMorgan's Kinexys for euro-denominated payments, part of a platform processing $2 billion daily.

The yield angle is driving treasury interest as fast as the liquidity angle. The tokenized Treasury market reached $5 billion in March 2025, offering yields of 4.8%-6.8% through instruments like BlackRock's BUIDL ($1.7 billion AUM) and Circle's USYC ($1.54 billion AUM). Corporate idle cash in traditional bank accounts earning near-zero interest can earn 3.7%-6.8% through on-chain Treasury exposure with 24/7 settlement flexibility. PayPal now offers 3.7% yield on PYUSD balances - a direct bid for enterprise treasury deposits.

Payroll and Contractor Payments

Global HR platforms now treat stablecoin payroll as a production feature. Remote launched USDC payments for contractors in 69 countries on Base. Deel, the largest HR platform by payroll volume, launched its stablecoin feature in February 2026. Rise Works offers USDC payroll with ADP integration.

Companies operating 50-person remote teams report saving $2,000-5,000 per month on transaction costs. Contractors in emerging markets who previously waited weeks for international wire transfers now receive payment in hours, in a currency that holds its value.

Settlement and Clearing

Visa launched USDC settlement for US banks in December 2025, settling on Solana. Initial participants include Cross River Bank and Lead Bank, with broader US availability planned throughout 2026.

Mastercard's acquisition of BVNK for up to $1.8 billion positions it for the same transition. In December 2025, SWIFT, HSBC, and Ant International completed a proof of concept for cross-border transfer of tokenized deposits using ISO 20022 standards, with over 30 financial institutions engaged.

AI Agent Payments

Autonomous AI agents need to make micropayments - for data access, API calls, compute, and storage - at frequencies and granularities below credit card thresholds. They operate 24/7, need programmable money without volatility, and cannot sign up for bank accounts. Stablecoins are the only settlement layer that fits.

Circle and Coinbase launched the x402 micropayments standard for AI agents in 2025. IBM, Stripe, and PayPal are all building for agentic payment use cases. Industry analysts cite agentic AI as a key driver of projected 56% stablecoin supply growth to $420 billion in 2026. This category of financial demand has no traditional finance equivalent.

Supply Chain Finance

Smart contract-based escrow replaces manual invoice processes for international trade. Funds release automatically upon delivery milestones, shipment confirmation, or customs clearance - eliminating payment timing disputes and freeing up working capital for suppliers. Corporate treasurers report 300-500 basis points of cost savings on international payments through stablecoin settlement.

The Multi-Chain Reality

Enterprise stablecoin operations span multiple blockchains. Each chain serves different geographies, cost profiles, and performance requirements.

| Chain | Stablecoin Supply | 30-Day Transfer Volume | Finality | Avg. Cost per Tx | Primary Enterprise Role |

|---|---|---|---|---|---|

| Ethereum | $161B (USDC dominant) | $2.09T | ~6 seconds | $1-5 | Institutional settlement, DeFi integration |

| Tron | $79B (USDT dominant) | $714B | ~3 seconds | <$0.01 | Emerging market B2B, Asia-Pacific remittances |

| Solana | $16B | $500B | ~400ms | <$0.01 | High-speed settlement, Visa USDC |

| Base | $4.6B | Growing | ~2 seconds | <$0.01 | EVM payroll, JPM deposit token, contractor payments |

| Arbitrum | Growing | Growing | ~2 seconds | <$0.05 | Enterprise DeFi, yield applications |

| Tempo | Launching | Early | <1 second | <$0.001 | Stripe payments, agentic micropayments, merchant payouts |

Ethereum is where institutional money settles - $161 billion in stablecoin supply and $2.09 trillion in 30-day transfer volume make it the default for large-cap USDC flows. Tron handles 60% of global stablecoin payment volume, driven by USDT-denominated B2B settlement across Asia where low transaction costs matter more than EVM compatibility. Solana is where Visa chose to run its US USDC settlement, drawn by 400ms finality and sub-cent costs. Base is where JPMorgan deployed its deposit token and Remote pays contractors in 69 countries.

Tempo adds a new dimension: a payments-native chain backed by the company that processes payments for millions of internet businesses. With 100,000+ TPS, sub-second finality, and a dedicated payments lane that separates routine transfers from complex smart contract operations, it is purpose-built for the stablecoin workloads that existing chains handle as a secondary use case.

An organization running cross-border supplier payments, treasury management, and contractor payroll simultaneously operates across at least three of these networks - and the number is growing.

What Comes Next

Five forces will define the next phase of enterprise stablecoin growth.

Bank-Issued Stablecoins

Wells Fargo's WFUSD, JPMorgan's deposit token, and the potential Zelle consortium stablecoin represent a new class of bank-native digital dollars. When the institutions that hold most of the world's deposits start issuing their own stablecoins, the volume flowing through on-chain rails accelerates with deposit-base economics, not crypto-market economics.

Agentic AI Settlement

Autonomous agents making micropayments for compute, data, and services generate transaction patterns that credit cards and wire transfers cannot serve - thousands of sub-dollar payments per hour, 24/7, without human intervention. This is a net-new category of financial activity with no traditional-finance equivalent.

Non-USD Stablecoins

EURC volume grew 76% month-over-month on average through H1 2025, rising from $42.5 million in June 2024 to $7.4 billion by June 2025. MiCA compliance is accelerating European enterprise adoption of euro-denominated stablecoins for intra-EU settlement. The stablecoin market is becoming multi-currency.

RWA Tokenization

Real-world asset tokenization exceeded $29 billion in on-chain value by September 2025, spanning 274 issuers and 385,000+ asset holders. Every tokenized Treasury, private credit instrument, and real estate asset needs stablecoins to purchase, redeem, and trade. Tokenized private credit alone exceeded $18.91 billion. As RWA tokenization grows, stablecoin settlement volume grows with it.

The Generational Demand Curve

The $100 trillion transfer from Boomers to crypto-native generations plays out over two decades. This is a sustained, compounding shift in who controls capital and how they choose to move it.

Chainalysis projects stablecoin transaction volumes could match Visa and Mastercard's combined off-chain volumes between 2031 and 2039. Nearly 1 in 4 North American CFOs say their finance functions will use digital currency within two years. The question is no longer whether stablecoins replace correspondent banking for cross-border settlement. It is how fast.

Frequently Asked Questions

Why are enterprises adopting stablecoins in 2026?

Regulatory clarity (GENIUS Act, MiCA), traditional finance participation (JPMorgan, Visa, Stripe, and major banks are all building), and measurable business value (up to 99% cost reduction on cross-border payments, settlement in seconds). Fireblocks found 49% of institutions actively use stablecoins for payments, with another 41% in pilot or planning stages.

How do stablecoins reduce cross-border payment costs?

Traditional correspondent banking charges $25-35 per transaction and routes through multiple intermediary banks over 2-5 days. Stablecoins settle peer-to-peer on a blockchain in seconds at transaction costs ranging from fractions of a cent (Tron, Solana, Base) to a few dollars (Ethereum). KPMG found the cost reduction can reach 99%. Speed is now the top driver - 48% of enterprises cite settlement speed over cost savings (30%).

What is the GENIUS Act?

The Guiding and Establishing National Innovation for US Stablecoins Act, signed July 18, 2025, is the first US federal framework for payment stablecoins. It requires 100% reserve backing with liquid assets, monthly public disclosures, and AML compliance. It passed with broad bipartisan support (68-30 Senate, 308-122 House) and gave enterprises the regulatory clarity to deploy stablecoin operations at scale.

What is the best blockchain for enterprise stablecoin payments?

It depends on the use case. Ethereum handles the largest institutional USDC flows ($161B supply). Tron dominates USDT-denominated B2B payments in Asia and emerging markets. Solana offers 400ms finality and is where Visa settles USDC for US banks. Base provides low-cost EVM compatibility for payroll and deposit tokens. Most enterprises need to operate across at least 2-3 chains simultaneously.

How fast do stablecoin payments settle?

Solana settles in approximately 400 milliseconds. Base and Arbitrum settle in about 2 seconds. Tron settles in about 3 seconds. Ethereum reaches finality in roughly 6 seconds. All of these compare to 2-5 business days for traditional correspondent banking wire transfers.

How big will the stablecoin market get?

Bernstein projects $4 trillion in total supply by 2035. Treasury Secretary Bessent has projected $2-3.7 trillion by end of decade. Chainalysis models adjusted transaction volume reaching $719 trillion by 2035 through organic growth, and up to $1.5 quadrillion with generational wealth transfer and point-of-sale adoption factored in.

For teams building on stablecoin-relevant chains, Dwellir provides multi-chain RPC infrastructure with archive node access and transparent pricing. Get started or talk to the team.